Inflation and Debt Delinquencies: The State of the US Consumer in early 2026

The US economy entered 2026 on solid footing, with consumer spending continuing to be the driving force behind macroeconomic growth. As the year unfolds, two factors will play a major role in determining whether the consumer-led momentum in the macro environment persists: inflation and debt delinquency. An objective assessment of these factors is provided below to examine how these factors will influence the likely trajectory of the economy, and the laundry industry, for the rest of 2026.

The US economy entered 2026 on solid footing, with consumer spending continuing to be the driving force behind macroeconomic growth. As the year unfolds, two factors will play a major role in determining whether the consumer-led momentum in the macro environment persists: inflation and debt delinquency. An objective assessment of these factors is provided below to examine how these factors will influence the likely trajectory of the economy, and the laundry industry, for the rest of 2026.

Inflation

The latest inflation data from the Bureau of Labor Statistics (BLS), which covered price changes through January 2026, exceeded most economists’ expectations, resulting in celebration across the financial media. The top-line read for the overall Consumer Price Index (CPI) reflected a 2.4% year-over-year increase, while the Core CPI (excluding volatile food and energy costs) was a bit higher, rising by 2.5% on an annual basis. These readings represent a notable decrease in inflationary pressure from just a few months ago, when overall prices were growing by 3.0% or more year on year.

However, there’s more depth to the data than just the top line numbers, and the devil – as always – is in the details. Firstly, the headline figures mask flaws in the data collection process. Due to the lack of reporting in October and November stemming from the longest government shutdown on record, the BLS had to “extrapolate” the numbers for those months. The process led to a lack of confidence in the validity of inflation data, at least in the near-term, for much of the economic community.

Inflation

The latest inflation data from the Bureau of Labor Statistics (BLS), which covered price changes through January 2026, exceeded most economists’ expectations, resulting in celebration across the financial media. The top-line read for the overall Consumer Price Index (CPI) reflected a 2.4% year-over-year increase, while the Core CPI (excluding volatile food and energy costs) was a bit higher, rising by 2.5% on an annual basis. These readings represent a notable decrease in inflationary pressure from just a few months ago, when overall prices were growing by 3.0% or more year on year.

However, there’s more depth to the data than just the top line numbers, and the devil – as always – is in the details. Firstly, the headline figures mask flaws in the data collection process. Due to the lack of reporting in October and November stemming from the longest government shutdown on record, the BLS had to “extrapolate” the numbers for those months. The process led to a lack of confidence in the validity of inflation data, at least in the near-term, for much of the economic community.

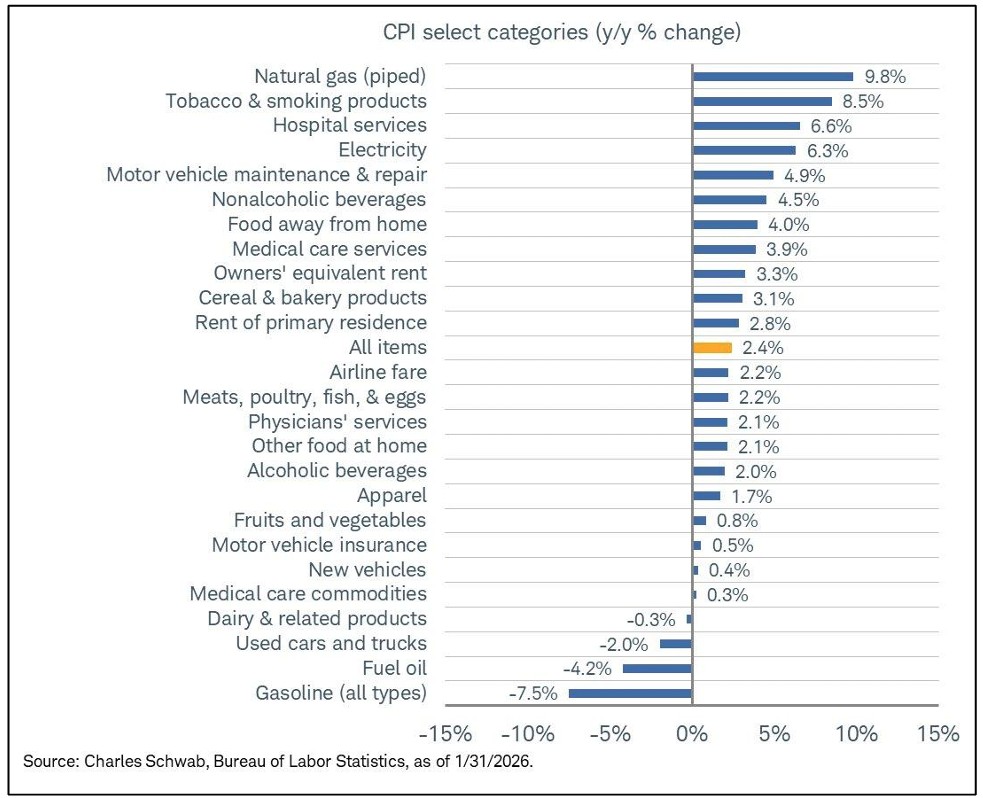

Furthermore, while the topline numbers looked good, and some product categories saw outright price declines (gasoline, used cars), most consumers feel like prices are growing at a substantially faster rate, and for good reason. As evident in the detailed chart below, there are many spending categories that buyers are faced with on a daily basis where prices are rising substantially faster than the overall average. For example, prices for energy services (electricity and natural gas) are up 7.9% over the past year, personal care costs are up 5.4% year-over-year, food away from home (eating out at restaurants) costs 4.0% more than it did a year ago, and medical care costs are 3.9% higher over the last 12 months.

Debt Delinquencies

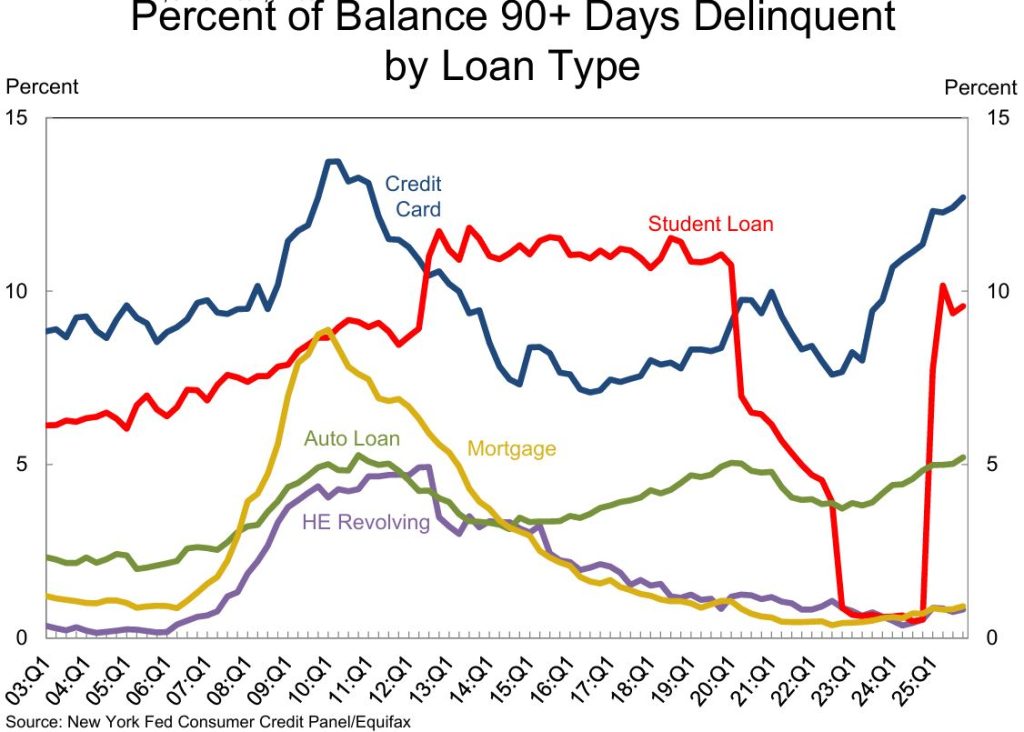

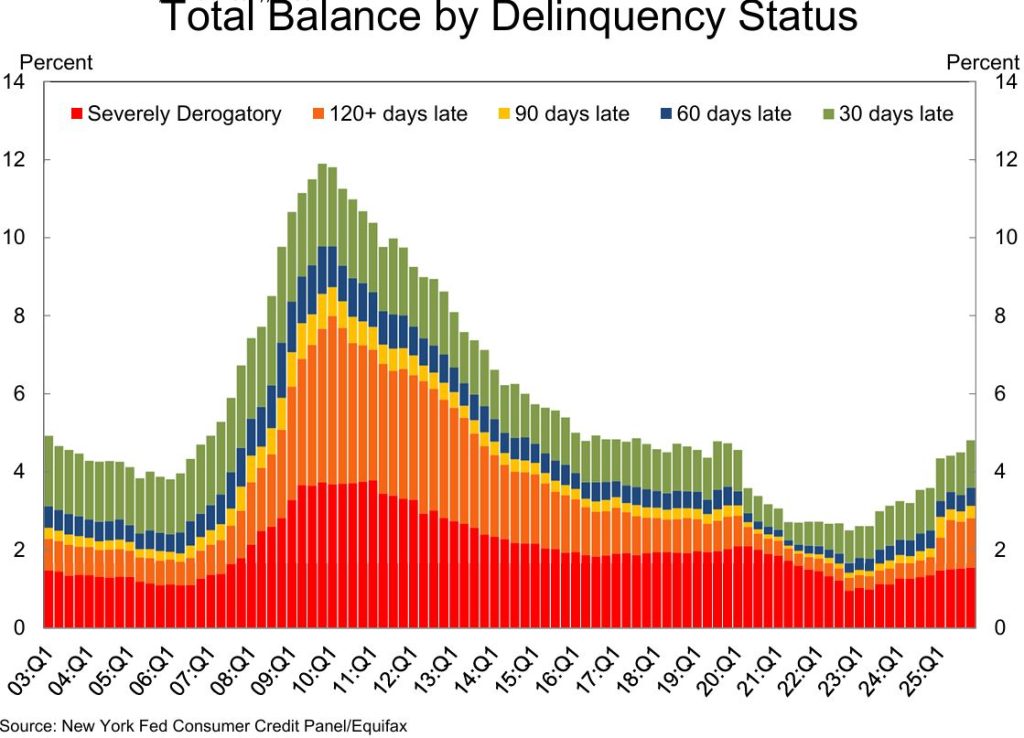

The Federal Reserve Bank of New York releases a quarterly report on the state of household debt and credit. The latest figures on delinquency rates, which provide coverage through the end of 2025, are worrying, with aggregate delinquency rates worsening in the fourth quarter of last year. At the end of December, 4.8% of all outstanding debt was in some stage of delinquency, 0.3 percentage points higher than in Q3 of 2025.

A few data points in the report were of particular concern. First, the share of credit card debt 90+ days overdue, which rose to 12.7% in Q4 of 2025, was at the highest level since 2011. In addition, auto loans have 5.2% of the total balance 90+ days past due. That’s the second highest quarterly rate ever, trailing only Q4 of 2010. In other words, both credit card and auto loan delinquencies are approaching levels that haven’t been seen since the Great Recession.

Transition into serious delinquency is highest for young consumers (18-29), while the next age bracket (30-39) also appears to be under substantial distress. Those in the later stages of their careers (40-59) seem to be doing notably better, with serious delinquencies remaining near levels seen before the pandemic. Rising delinquencies are most prominent in states that had red-hot housing markets post-Covid and have since cooled, like Arizona, Florida, and Texas.

However, not all the news in the debt and credit report is grim. While transition into early delinquency ticked up slightly for mortgages and more significantly for student loans, it held mostly steady for autos, credit cards, and HELOCs. The transitioning rate into serious delinquency for those 18-29, an age group that represents the most prominent customer growth category for laundry operators, slowed over the past year for most debt types with one glaring exception: student loans.

In addition, while the delinquency data clearly shows that consumers are in a state of elevated financial stress, recent retail sales performance points to spending behavior that is bending rather than breaking. In other words, consumers are still out there spending money, they just demand more quality and value for their hard-earned cash. The focus for laundry operators in 2026 should be laser-focused on delivering customer value, quality, and an exceptional customer experience.

Related Posts

-

PodcastCuriosity and Mentors Make the Difference for Two Women in Laundry Service

In this episode of Full Cycle, Matt DeWolf sits down with two women who have built long careers on the service and maintenance side of the laundry industry: Jennifer Gonzalez, Senior Manager of Servic…

2 min read -

Member SpotlightBuilding for the Long Run: How One Long Island Operator Turned Strategic Thinking into Three Thriving Stores

Joseph Musheyev didn’t stumble into the laundry business. The Long Island storeowner came in with intention, armed with research and a clear-eyed understanding that success in this industry depends as…

6 min read -

NewsCLA Advocacy Has Saved Laundromat Owners and Customers $7.4 Billion, Report Finds

Two decades of work in statehouses and Washington kept taxes, mandates and shutdown orders from raising costs across the industry

CLA Advocacy Has Saved Laundromat Owners and Custome…

3 min read